US May CPI

Starting with commentary BEFORE and then after

Estimates:

Firm - Headline ; Core

Barclays - 3.4%, 0.1%; 3.5%, 0.3%

BofA - 3.4%, 0.1%; 3.6%, 0.3%

BNP Paribas - 3.3%, 0.1%; 3.6%, 0.3%

Citi - 3.4%, n/a%; 3.5%, 0.3%

Deutsche Bank - 3.4%, 0.1%; 3.5%, 0.3%

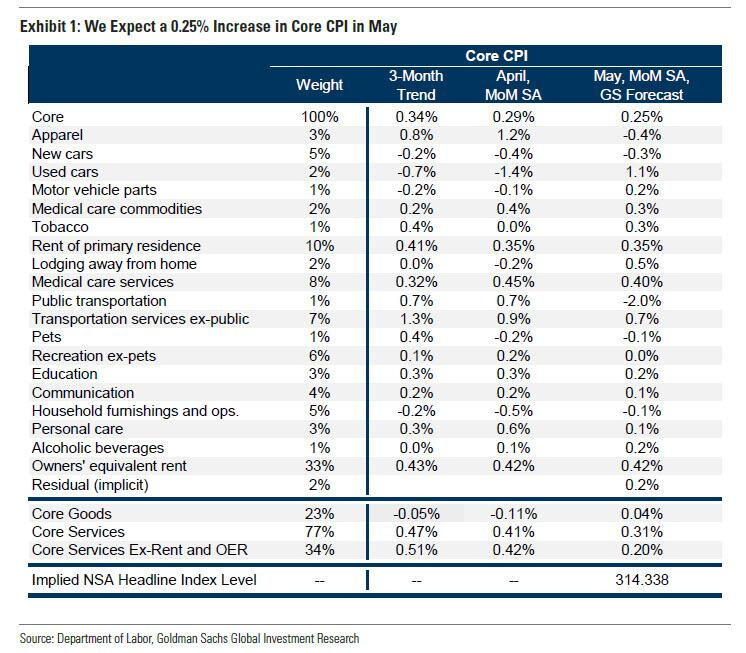

Goldman - 3.4%, 0.1%; 3.5%, 0.3%

HSBC - 3.4%, n/a%; n/a%, n/a%

JP Morgan - 3.4%, n/a%; n/a%, n/a%

Morgan Stanley - 3.4%, 0.2%; 3.5%, 0.3%

Nomura - 3.4%, 0.1%; 3.6%, 0.3%

Scotia - 3.5%, n/a%; n/a%, n/a%

TD - 3.3%, 0.1%; 3.5%, 0.3%

UBS - 3.4%, 0.1%; 3.5%, 0.2%

Wells Fargo - 3.4%, 0.1%; 3.5%, 0.3%

BofA

After averaging 0.4% m/m in January through March, inflation took a small step in the right direction in April with core Consumer Price Inflation (CPI) and Personal Consumption Expenditure Inflation (PCE) both decelerating to 0.3% m/m (core PCE inflation was 0.26% rounded to two decimals).

We think May follows suit and our forecast is for core and headline CPI inflation rising by 0.3% (0.30% to two decimals) and 0.1% m/m. This would leave core and headline up 3.6% and 3.4% y/y, respectively, both unchanged from April levels. We look for core goods prices to increase slightly changed on the month, while services inflation should show some modest improvement but remain sticky at 0.4% m/m.

Goldman (Econ team)

Goldman (Strategist)

Dom Wilson (Senior Markets Advisor): The combo of a CPI release and an FOMC with a fresh SEP is obviously a key event risk and creates the potential for a decent amount of intra-day movement too. Our baseline forecasts (0.25% on core CPI with an eye into a 0.19% on core PCE and a 2-cut median dot for 2024) are likely to be a source of at least modest relief, and the news since the May FOMC suggests that Chair Powell should not sound too different from the last press conference. The market is still worried about the extent of progress on the inflation side and I think there are plenty of people expecting a 1-cut Fed dot, so avoiding those more hawkish outcomes should deliver some upside to risk assets. You’ve also got a somewhat higher vol profile for the day than in some prior months, which suggests more focus/nervousness on these events. I think you need a core inflation reading above 0.3% to create a real challenge, and a 1-cut 2024 dot – even though it won’t really be unexpected - would probably also create some renewed upward pressure on yields and downside for equities. Our core view has remained positive on US stocks, while using cheaper optionality to protect against event risk, so the basic strategy hasn’t changed. There isn’t as clear an opportunity here as we sometimes see, but I think the current set-up favors calls or call spreads. With very near-dated vol elevated it may make sense to avoid very short-dated tenors, which have often looked particularly attractive for these events. And we’ve also started to think about more medium-term protection opportunities as the US election comes more firmly into focus. I think part of the challenge is that the calendar beyond here doesn’t create an obvious runway for extended relief, particularly with European political noise picking up. You’ve also got the BOJ behind this and beyond that the focus turning to the first Presidential debate - we’ve generally liked using the recent weakening in the USD to set up some medium-term long USD exposure for the coming month, though the European election surprises have meant that entry points in spot and vol are not nearly as good as last week.

Joe Clyne (US Index Vol Trading): Heading into FOMC/CPI, short-dated vols have retraced back towards the lows of the year (excluding the very end of May). S&P 1 month 25 delta call vols are trading on a single digit vol handle which is more than a vol below its one year average. Interestingly, we are still seeing substantial vol inversion between June and July with the rich event calendar over the next few days. The combination of the vol inversion, the low vol further out the curve, and the substantial dealer long gamma positioning leads to us liking long vol trades better than long gamma trades over the course of this week. The straddle for CPI/FOMC itself looks to go out around 1% which certainly isn’t egregious, but you would need both events to surprise in the same direction to substantially outrealize that straddle. In the short-dated space, we like SPY July call spreads to play for further upside and, in the belly of the curve, we think 4 month SPY vol is the most attractive area to go outright long vol as it approaches post-2017 lows.

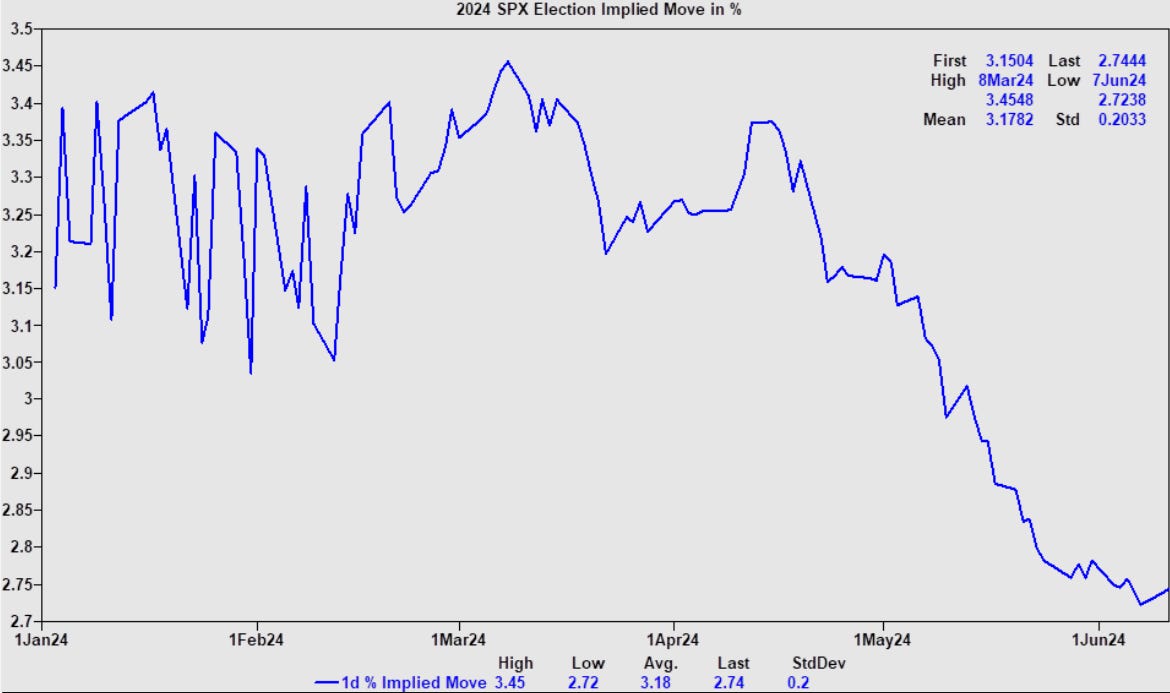

Shawn Tuteja (Macro EQ Vol Trading): Our sense from client conversations is that there is optimism for a low CPI print, and we think that's helped provide support for broader equities (excluding RTY / cyclicals / banks) on this most recent leg higher in bond yields. We’re watching as to whether clients use a low CPI print as a way to reduce overall portfolio risk. GS PB shows nets in the 99th percentile now on a 1y lookback (70th on a 5 year lookback), with grosses at historical highs, yet clients continue to remain constructive equities in light of a friendly FOMC committee and mixed data thus far. While much has been made of SPX implied volatility reaching new lows, this vol pressure has spilled into other assets and themes. We think there are opportunities to buy implied volatility on cyclicals and high leverage EQ names that have yet to fully price in the effects of insurance cuts coming out of the rates curve. Our view is that after the CPI/FOMC, clients will start to turn their focus to the elections, which have historically led to risk-reduction. In 2016, SPX corrected almost 9% from early Sep to end of Oct (and almost 5% over the same timeframe in 2016), and both of the previous elections have seen implied vol squeeze into them. Our internal model shows a 2.74% implied move (1.9% of which is “extra” variance) already for the election, and the first debate is on June 27th.

JP Morgan

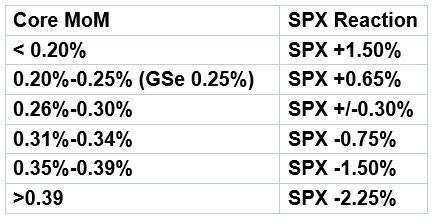

Above 0.4%. The first tail-risk scenario, this outcome is likely achieved by an increase in both Core Goods and Core Services, with Core Goods flipping from deflationary to inflationary MoM. Within Core Services, we would likely see shelter inflation increase. The bond market reaction would likely be a 12-15bps increase as part of a bear flattening. Equities would react negatively to this repricing. Given the acceleration higher in inflation, rate cut bets for 2024 would evaporate and we will see the return of views of a rate hike. This would be exacerbated by any comments from Powell suggesting rates are not restrictive enough. Probability 5%, SPX falls 1.5% to 2.5%.

Between 0.35% - 0.40%. This outcome is likely achieved by a smaller than expected disinflationary impulse from Core Goods with Shelter remaining flat. Bonds react negatively as Sept/Nov rate cut views decrease. With market fixings pricing in ~0.26% for Core MoM, the bond market reaction could be larger than expected with many Equity investors focused on the surveyed number of 0.3%. Probability 15%, SPX falls 1% to 1.25%.

Between 0.30% - 0.35%. This scenario has the widest range of outcomes since the low end of the range supports the disinflationary trend and the higher end of the range the stickier inflation argument. Feroli’s forecast for 0.33% would keep the YoY number flat from last month’s print. The biggest drivers are weak disinflation in shelter, increases in vehicle, medical, and communication prices. Given the move in bond yields on Friday (+14.6bps to 4.43%), there is likely a more muted response to a hotter print. Also referencing Friday, it was surprising to see stocks slough off the bond market move with the SPX falling only 11bps instead of 1%+ as we have seen over the last couple years in response to significant and sudden moves in bond yields. Probability 40%, SPX loses 0.75% to gains 0.75%.

Between 0.25% - 0.30%. As mentioned, the market fixing implies a 0.26% core reading and the move in yields may not be as strong as one would expect on a beat where one would expect ~15bps move in the 10Y yield but this is a positive outcome for risk assets as this print would likely restart the Goldilocks narrative with 24Q1 data being viewed as an anomaly. Probability 25%, SPX gains 0.75% to 1.25%.

Between 0.20% - 0.25%. The immediate reaction would be a surge in September rate cut expectations with some likely pointing to July for a surprise, insurance cut given the move by the ECB. While July sees highly unlikely, putting September back on the table would be view favorably by risk assets and we could see some yield curve steepening to aid the Cyclicals/Value trade. Probability 12.5%, SPX gains 1.25% to 1.75%.

Below 0.20%. Another tail-risk scenario, likely fueled by a material decline in shelter inflation with goods disinflation supporting the print. Look for a collapse in yields, a material increase in July cut expectations, and a rally across all risk assets ex-commodities. In Equities, this would look like an “everything rally” with both NDX and RTY outperforming the SPX. This outcome, if confirmed in the July print, would trigger a reset in thinking about which stage of the economic cycle we currently reside as well as talks of the Fed having achieved a No Landing/Soft Landing scenario. Probability 2.5%, SPX gains 1.75% to 2.50%.

Tactically bullish. We think the 0.3% - 0.35% scenario is what unfolds. As we continue to wait for a ‘catch down’ between official housing pricing and real-time indicators, we are seeing other elements increase their inflationary impulse such as medical services and vehicle prices. This year, core prints have surprised hawkishly (3 of 5 prints) or been in line with survey (2 of 5 prints). The combination of this print with a neutral/dovish Powell press conference means that we would buy any dip created by this event. Our bullish view (at/above trend GDP + positive earnings growth + paused Fed) remains intact and the bull case gets additional support from the AI-theme which has two more data points this week in AAPL and AVGO. With 2 US holidays over the next 4 weeks, we may see volume declines lead to larger than expected moves despite an information vacuum after this week.

Monetization menu: Tech has been the only major sectors that has outperformed on both a 1-week and 1-month basis, highlighting narrowing breadth. I think we need to see either a pullback or a shift in how the market views economic fundamentals to see market breadth return. For that to occur with this week’s events, we would need a dovish CPI print and a dovish Powell who highlights broad economic strength that is accelerating, e.g., growth without inflation. MegaCap Tech remains the “safest” long but keep an eye on Healthcare and Consumer Discretionary as other long plays if we fail to see a narrative shift. In a market broadening scenario, Energy, Financials, and Industrials are the long plays that I would add.

Morgan Stanley

We forecast core CPI inflation at 0.28%M in May (3.5%Y) on lower services inflation.

Data in line with our expectation point to May core PCE at 0.22%M from 0.25%M in April. We expect headline CPI at 0.146%M due to negative energy inflation.

Nomura

Wells Fargo

Inflation will be back in the spotlight next week with the release of May’s CPI report on Wednesday.

We anticipate the report to provide additional evidence that inflation is returning to a cooling trend after flaring up in Q1.

Although food prices likely picked up slightly, lower oil prices should translate to a decline in energy prices during the month, helping yield a soft reading on the headline.

Goods prices likely fell again, driven by declines in vehicle, apparel, recreation and household goods prices.

Meanwhile, services prices look to have increased for a second straight month amid the slow moderation in shelter costs and other services inflation.

Altogether, we estimate that the headline CPI increased 0.1% during May, which would amount to a 3.3% year-over-year rise.

In terms of core CPI, we look for a 0.3% monthly gain and a 3.5% year-over-year increase.

As of this writing, our forecasts for headline and core CPI are generally consistent with the Bloomberg consensus.

The results of May’s CPI release are not likely to have a meaningful impact on the outcome of the FOMC meeting next week, although Fed officials will no doubt be paying close attention.

Results expected at 8:30AM ET. Read live commentary here when it comes out