Goldman Sachs: Trading Desk 06/11/2024

S&P +27 basis points closing at 5375 with a MOC: $1.4 billion to SELL. NDX +71 basis points at 19210, R2K -36 basis points in 2024 and Dow -31 basis points at 38747. 10.6 billion shares were traded across all US stock exchanges compared to a ytd daily average of 11.5 billion shares. VIX +86 basis points at 12.85, Crude +12 basis points at 77.83, 10-year yields -7 basis points at 4.39, gold +23 basis points at 2316, dxy +11 basis points at 105.26 and bitcoin -316 basis points at 67400 .

**SPX and NDX closed at new all-time highs today, although it certainly didn't look like it with only 185 names ending in green. Stocks bounced back from early weakness on falling yields (healthy 10-year bond auction) + APPL rally +7% for 1) sell-side positive on WWDC overnight (improvement + rise from GIR PT to $238, link), 2) retail commitment (highest call option volume of the year) and 3) Material increase in L/O adds in recent weeks. Elsewhere, banks were weak on disappointing commentary coming from industry conferences. The ADRs were sold by this headline: US CONSIDERING MORE LIMITATIONS ON CHINA'S ACCESS TO CHIPS NEEDED FOR AI.

Our desk was a 4 on a scale of 1 to 10 in terms of overall activity levels. Flows were relatively subdued out of Technology and Healthcare as we await CPI/FOMC tomorrow. Day 2 of the GS HC Conference was decidedly more micro/volatile focused compared to day 1, with a number of intraday swings due to updates throughout the day. The overall executed flow on our desk ended with a buying bias of +562 basis points today compared to a 30-day average of +190 basis points. Long-term orders (L/Os) ended as net buyers by +24%, adding a ~$2 billion increase in incremental demand in Technology (HIGHLY concentrated in AAPL), followed by communication, industrial and financial services. Hedge funds (HFs) finished as net buyers at +170 basis points driven by demand in technology and macro products compared to supply in Finance and Healthcare.

DERIVATIVES: Lower volume in the derivatives space ahead of tomorrow's catalysts as short-term volumes rose slightly despite remaining near ytd lows. The flows consisted primarily of short-term RSP/IWM rallies, as well as some SPX hedging in the space of 3-6 months. In the individual stock space, 2.9 million Apple call options were traded compared to the 20-day average of 570k, as the stock hit all-time highs. For tomorrow, the options market is implying a move of around 95 basis points. To put this in context, the CPI's average move is 80 basis points, the FOMC's average move is also 80 basis points, and the daily average move is 60 basis points. (h/t Braden Burke)

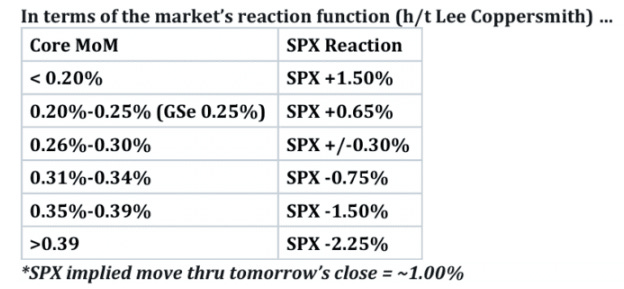

Before the CPI

We expect a 0.25% increase in the core consumer price index (CPI) for May (vs. 0.3% consensus), corresponding to a year-over-year rate of 3.50% (vs. 3.5% consensus); link. We highlight three key trends at the component level that we expect to see in this month's report:

We expect a slower pace of inflation in consumer electronics, personal care and other consumer products, reflecting price declines in the Adobe data set and consistent with price reductions announced by large retailers.

We expect auto insurance prices to continue rising but the pace of increases to slow. We forecast a 1% increase in the auto insurance component, compared to 1.8% in April and 2.6% in March.

We expect rent and OER (owner equivalent income) inflation to remain stable at 0.35% and 0.42%, respectively, reflecting a normalization in the pace of rent growth for new tenants and a greater difference between rents for new tenants. and existing tenants in single-family units, which have greater weight in the OER than in the rental market in general.

Looking ahead, we expect monthly core CPI inflation to remain in the 0.2-0.3% range over the next few months before stabilizing around 0.2% by the end of 2024.