Goldman Sachs: Trading Desk 03/06/2025

U.S. futures hit record lows – the 10-year U.S. Treasury yield fell to 4.29% – as weakness in the tech sector weighed on market sentiment.

Alibaba has launched its new DeepSeek competitor , which reportedly uses only ~5% of the data units that DeepSeek's low-cost model employs.

Marvell Technology (MRVL) falls -15% and MongoDB (MDB) -18% following their earnings reports.

Recent headlines about tariffs are also impacting market sentiment.

The S&P 500 has its 200-day moving average at 5728 as a key downside level , while CTA supply remains a key factor in market dynamics.

The ECB is expected to cut rates by 25 basis points later this morning.

In Asia, stock markets closed higher, driven by the technology and AI sectors in Hong Kong, following the Alibaba news ( +8% locally , Tencent +7% ).

In Europe, the picture is mixed :

Germany continues to shine after yesterday's fiscal expansion announcements.

European leaders meet in Brussels to work on defense spending plans .

EU retail sales and the UK construction PMI were worse than expected.

The S&P 500 looks poised to break above the 200-day moving average (5728) this morning…

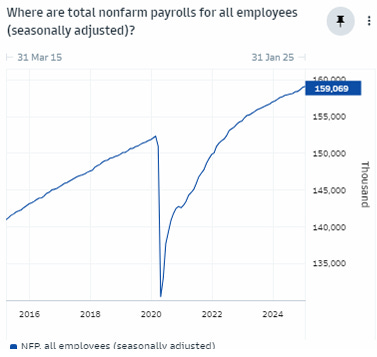

NFP PREVIEW…

Goldman Sachs (GS) continues to expect a figure above consensus, with a forecast of +170,000 jobs.

FOCUS ON FACTORS – MARKET ACTIVITY

Our desk closed with +334 bps as net buyers, compared to an average of +30 bps over the past 30 days. Despite the movements, trading activity felt subdued.

Long-term investors (LTOs) were net buyers of $1.7B , driven by demand in technology, consumer discretionary and utilities , with lower supply in healthcare and industrials .

Hedge funds (HFs) ended as small net buyers (+$300M) , with demand in consumer discretionary , but selling in technology and energy .

COAL… The coal rally is underway

Coal prices are poised for a comeback as strong demand meets stagnant supply. Although the world will eventually transition away from the most polluting fossil fuel , its short-term popularity appears assured . (Source: Bloomberg)

CTA… Vendors in the market

According to yesterday's data, expected sales for the next 7 days are:

If the market remains stable: $53.88B in sales ($36.52B outside the US).

If the market rises: $37.10B in sales ($26.42B outside the US).

If the market goes down: $74.64B in sales ($36.27B outside the US).

TARIFFS… Trade uncertainty hits U.S. consumers

The tariff swings are scaring American consumers. Uncertainty surrounding Trump's trade war is affecting purchasing behavior, causing some consumers to cut back on spending. (Source: WSJ)

SPX… Intraday volatility at record highs

SPX intraday bands are at their highest level since the carry trade liquidation in August…

AI Spending… Goldman Sachs on Why AI Spending Isn't Boosting GDP

1. Annualized revenue of public companies exposed to AI infrastructure increased by more than $340 billion between 2022 and the fourth quarter of 2024, and is projected to grow by nearly $580 billion by the end of 2025. However, actual annualized investment in AI-related categories within U.S. GDP accounts has only increased by $42 billion over the same period. This marked divergence has raised questions among investors about why U.S. GDP is not receiving a bigger boost from AI.

2. Margin expansion (+$30 billion) and increased revenue from abroad (+$130 billion) are estimated to account for about half of the AI spending boom reported by public companies.

3. However, the BEA ’s methodology may underestimate the impact of AI investment on real GDP by around $100 billion . Manufacturing shipments and net imports suggest that the US supply of semiconductors has increased by over $35 billion since 2022 , but the BEA classifies semiconductor purchases as intermediate inputs rather than investment , excluding these data from the GDP calculation.

4. Together, these factors largely explain the discrepancy in AI investment, leaving only $50 billion unaccounted for.

5. Looking ahead, AI investment is expected to have a modest impact on US real GDP in 2025 , as spending expands into categories such as data centers, servers, networking hardware, and utilities , which are counted as real investment.

6. However, most investment in semiconductors and cloud computing will remain unmeasured unless there are changes in the U.S. national accounts methodology.