S&P -1.37% close @ 4,953 with a Market Order of -$2.4bn to SELL. NDX -1.58% @ 17,600, R2K -4.16% @ 1,969 and Dow -1.35% @ 38,272. 12.9 billion shares were traded across all US stock exchanges versus the year-to-date daily average of 11.5 billion shares. VIX +13.8% @ 15.85, crude oil +107 basis points @ 77.74, 10-year yields +14 basis points @ 4.32%, gold -135 basis points @ 2005, dxy +68 basis points @ 104.88 and bitcoin -44 basis points @ 49,646 . Some pain and methodical selling pressure after this morning's strong CPI print with SPX -1.4%, NDX -1.6% and R2K -4.1% (worst session for IWM since JUN 2022). It was an undoing of the undoing in a moderate trading activity with the weakest links being hit the hardest: Most Short -5.5%, Non-Profitable Tech 5.3%, Short Momentum -4.1%,

Regional Banks -4.3% while Crowded Longs (GSPUCRWD) traded 'good' +85 basis points. Central CPI MoM increased +0.39% vs cons +0.3% and y/y rate remained unchanged at 3.9% vs cons 3.7%, driven by strength in job-dependent categories such as medical services, insurance and auto repair, and childcare that appears consistent with the January effect. Our economists still believe inflation in these categories returns to the previous trend in February and March and tentatively expect core PCE prices to rise 0.34% in January (mom sa). Even though all 57 of our thematic baskets closed lower today, it was the quietest day on our trading desk in over a week, although we were bombarded with questions. We do not believe that today was a turning point for a more sustained move lower from the ATH. The CPI fell somewhere between warm and hot. The March cut is officially off the table and May will remain up for debate (the market is showing a 26% chance for May right now). Our desk was a 4 on a scale of 1 to 10 in terms of overall activity levels.

The flow executed on our desk ended with a sell slope of -157 basis points vs a 30-day average of 75 basis points. We did not see deleveraging behavior on our desk that was overly concerning. We think that today's movements reflect that the market is giving back what was a fierce squeeze. L/Os ended -6% net sellers, driven by supply in semiconductors and macro products versus demand in industrials and discretionary products. HFs finished 1.6% net sellers after selling back the corners of the market that were squeezed the most. Short ratios were elevated in HC, Energy and Utilities.

After the close: LYFT +50%: went from +60% after the close to +12.3% now – typo in presentation on margin expansion… 50 basis points NOT 500 basis points! ABNB +9% (at 2-year highs in the trailing period), in line with Q4 in RNs but solidly outperformed in GBV and EBITDA well above the street at $738mn (33% margin) vs. cons $643mn ( margin of 30%). Q1 revenue guidance above street expectations + announces buyback of up to $6bn (vs ~$100bn market cap).

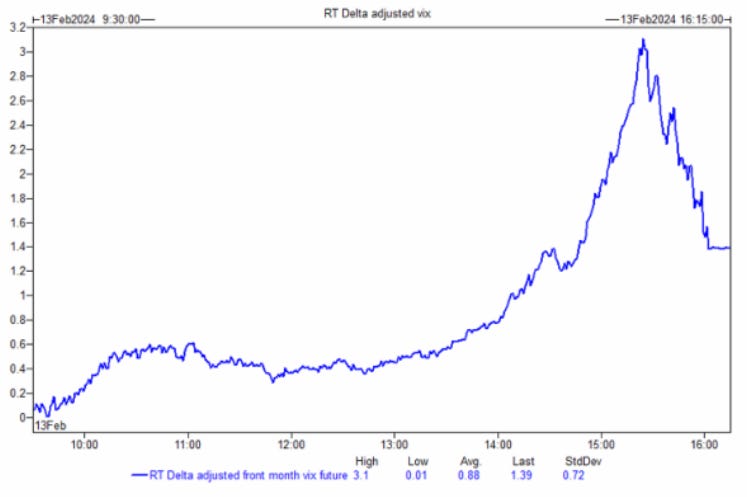

DERIVATIVES: Despite the selling today, flows on the volatility desk did not reflect a sense of panic. In the initial move after the CPI, some clients traded index puts and we had a buyer of the 20k Friday SPY 480-470 puts spread. Fixed price volatility was in demand later in the day and the VIX had its biggest one-day move since last March before selling off at the close. We also saw the second highest VIX call volume in the last 5 years with 1.76 million contracts. After making the 0.67% straddle today, the Friday afternoon straddle came out at 1.01%. (Braden Burke mention)