Goldman Sachs: Tesla - 3Q deliveries takeaways (10/02/2024)

Tesla delivered about 463k vehicles and produced about 470k vehicles in 3Q24

Tesla reported preliminary 3Q24 vehicle deliveries of about 463k (up 4% qoq and up 6% yoy), and production of about 470k (up 9% you).

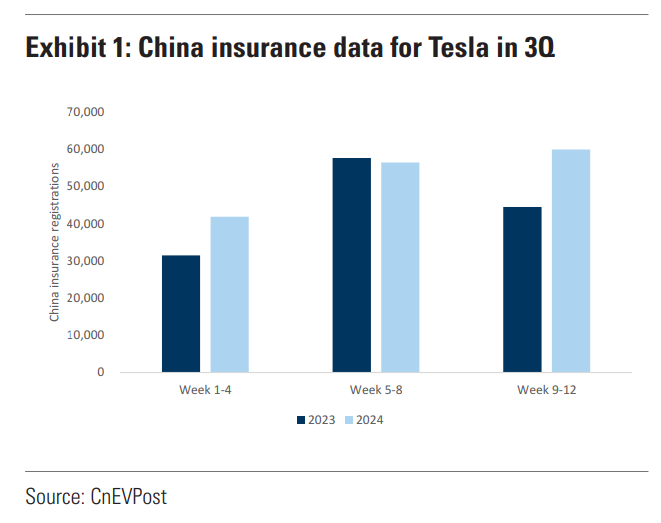

Deliveries of about 463k in 3Q24 were roughly in line with Visible Alpha Consensus at about 461k, and GSe at 460k. However, we believe some investors were expecting a modestly higher delivery number in part as China was relatively strong recently per insurance data (Exhibit 1). We believe growth in China in the quarter was partly offset by weakness in Europe.

Model 3/Y deliveries in the quarter were about 440k (up 4% qoq and up 5% yoy), and other model deliveries (e.g. S/X/Cybertruck) were about 23k (up 6% qoq and up 43% you).

Lease mix was 3% of deliveries in 3Q24 (vs. ~2% in 2Q24).

Separately, Energy storage deployments of 6.9 GWh were below our expectation of 9.6 GWh.

Implications and analysis

With the 3Q delivery data relatively in line, we expect the focus from investors from here to be on the following:

1) Tesla’s upcoming 10/10 “We, Robot” event: As we discussed in our 10/10 event preview note, we expect the robotaxi (or Cybercab) unveil and the company’s technology and business outlook for FSD/robotaxis to be a prominent part of the event. We expect Tesla will target to begin operating a robotaxi business next year in small scale based on the comments the company has made on the rate of progress that it is making, perhaps in a state like Texas, Arizona or Nevada were regulations and weather are more favorable (and where Tesla offers insurance). Whether Tesla can give investors more confidence on how well the FSD technology is working and the path forward will be a key focus item for investors in our opinion (e.g. showing intervention data). We also expect Tesla to emphasize a cost advantage in AVs given its design choices/sensor stack and scale, and potentially utilize its data and insurance operation to save on operating costs longer-term.

In addition, we would expect to learn more on Optimus, especially given the event title is “We, Robot”.

Finally, we’ll be interested if Tesla shares more on future consumer vehicles such as the lower-cost model planned to start shipping in 1H25, although some investors have argued a consumer vehicle unveil would have its own event and Tesla would not risk cannibalizing its current lineup.

2) Can the auto business grow more meaningfully in 2025: 3Q24 volumes returned to yoy growth, and 2024 volumes are tracking to be relatively flat yoy in our opinion (we assume -1% yoy). We believe a key debate in the market is now whether Tesla can grow more meaningfully in 2025/2026, driven by a refreshed Model Y and a new lower cost model(s). While it is unclear if Tesla will share more on this at the 10/10 event, whenever Tesla does provide more details on its new model(s), the degree that new features/costs are differentiated vs. what Tesla currently provides, and the ensuing impact on growth, is likely to be a key investor debate. While Tesla may somewhat cannibalize sales of the current 3/Y with new variants depending on the degree of differentiation, net net as new model(s) fully ramp we’d expect them to add at least 100K to Tesla’s annual volumes (as we discussed in our note “Framing the market size for lower cost vehicles”).

3) Automotive gross margin: We expect Tesla’s automotive non-GAAP gross margin excluding regulatory credits to remain a key focus for investors, and we’re modeling the automotive non-GAAP gross margin to be flat sequentially at 14.6% in 3Q. There are several puts and takes, including a full quarter of the financing incentives but also higher volumes, and we believe lower input costs.

4) Growth in other segments, including Services and Energy: Tesla deployed 6.9 GWh of energy storage products in 3Q, below the 2Q level of 9.4 GWh. Recall Tesla has previously noted that given the large-scale nature of some projects, deployments by quarter could be lumpy. We believe the lower shipments in 3Q qoq are likely due to lumpiness, and we expect Energy to grow as the company ramps capacity. However, with Energy now the company’s highest gross margin segment, we believe better understanding the outlook for Energy will be a topic on the upcoming 3Q earnings call. Recall that Tesla guided its full year Energy storage deployments to grow by >75%.

We maintain our 2024/25/26 deliveries estimates of 1.79 mn/2.10 mn/2.40 mn. We lower our 2024 EPS estimate including SBC to $1.80 from $1.87 prior reflecting lower Energy revenue and lower S/X vehicle mix (which carry higher ASPs).

We maintain our 2025/26 EPS estimates including SBC of $2.95/$4.20. Our estimates excluding SBC for 2024/25/26 are now $2.21/$3.35/$4.60. We maintain our 12-month price target of $230, which is still based on 65X applied to our Q5-Q8 EPS estimate including SBC.

We remain Neutral rated on the stock. While we believe that Tesla can grow longer-term including with FSD, we believe headwinds in the auto business (e.g. a high degree of competition and pricing pressure in EVs) will limit the rate of its EPS growth in the near to intermediate term, we expect it will take time to grow its FSD/software business to a more meaningful level, and we believe valuation is full.

Key downside risks to our view relate to potentially larger vehicle price reductions than we expect, increased competition in EVs, slower EV demand, delays with products/capabilities like FSD/4680, key person risk, the internal control environment, margins, and operational risks associated with Tesla’s high degree of vertical integration. Upside risks include faster EV adoption and/or share gain by Tesla, a stronger macroeconomic environment for new vehicle sales more generally, earlier new product launches than we expect, and an earlier/larger impact from AI enabled products (e.g., FSD, Optimus and robotaxis) than we currently anticipate.