Goldman Sachs: Can Gold Keep Rising?

Goldman Sachs: Can Gold Keep Rising?

China Gold Market Overview

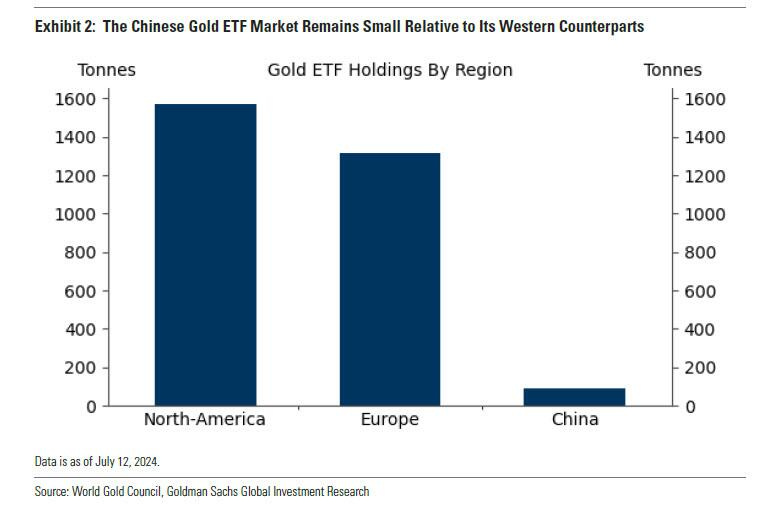

China’s strong tradition of owning physical gold and easy access to the metal mean that it remains the dominant form of demand. Although gold-backed ETFs are gaining ground in China, their market size remains small compared to their Western counterparts.

Demand for physical gold

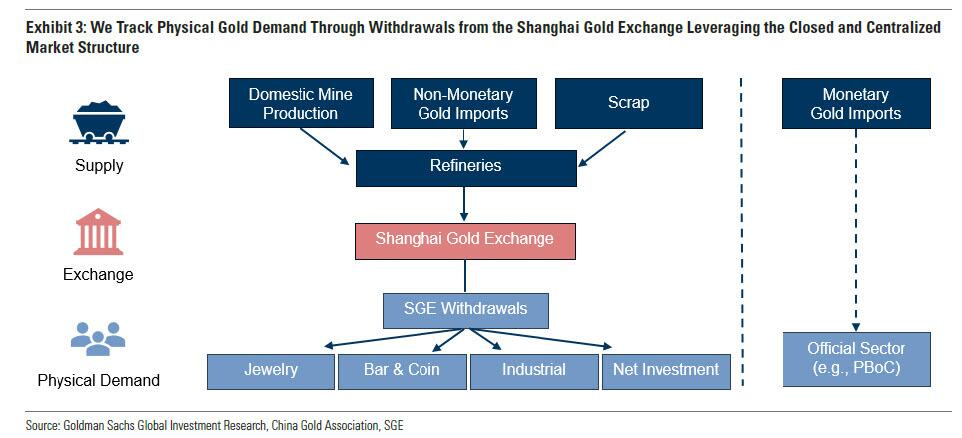

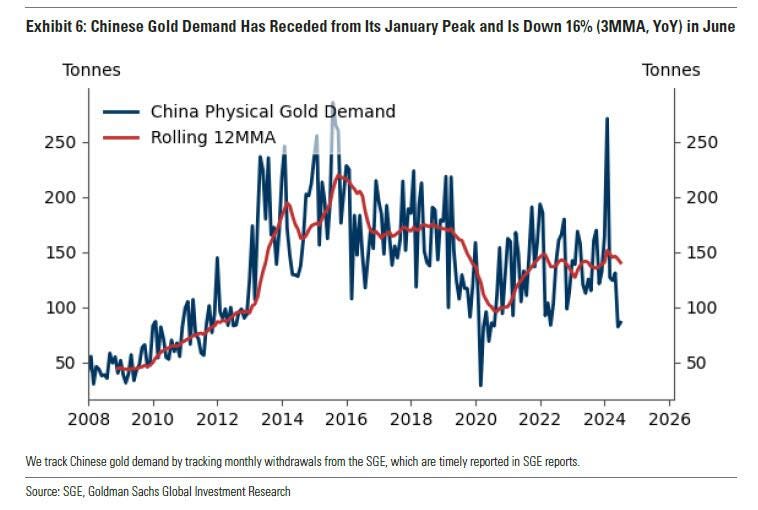

We can track the demand for physical (private) gold by tracking withdrawals from the Shanghai Gold Exchange (SGE), as it is a centralized closed market. Almost all physical gold transactions are done through the SGE due to its high liquidity, regulation, and tax incentives.

An exception is the official sector, including the People's Bank of China, which operates outside the EGS and buys gold directly on international markets that provide the liquidity needed for large transactions and allow payment in foreign currencies, unlike EGS contracts denominated solely in renminbi.

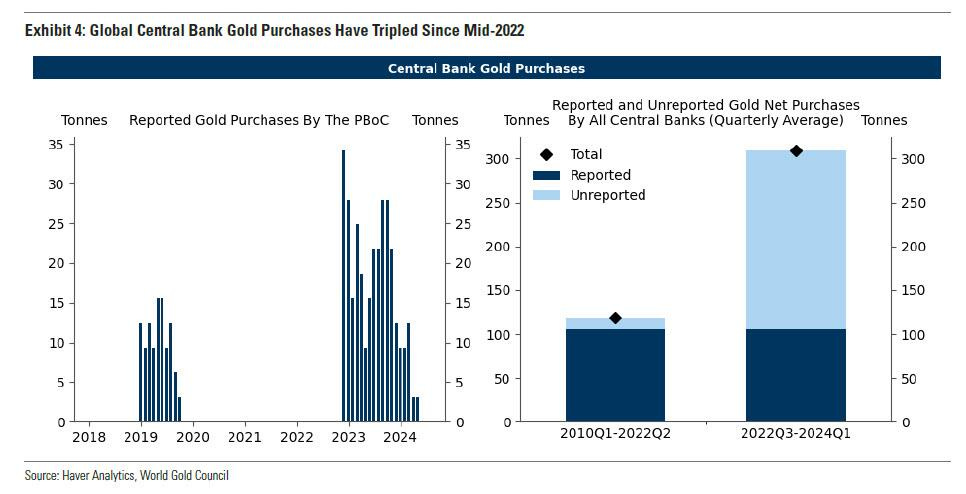

China’s central bank has reported 18 consecutive months of gold purchases as of November 2022, accumulating 317 tonnes. We have also shown that emerging market central banks have tripled their purchases since mid-2022 due to fears of US financial sanctions and concerns about that country’s sovereign debt, with most purchases now unreported. Despite a pause in China’s reported purchases for May and June, the reality is that emerging market central banks, including China, will continue to buy gold frequently, whether disclosed or not.

Supply

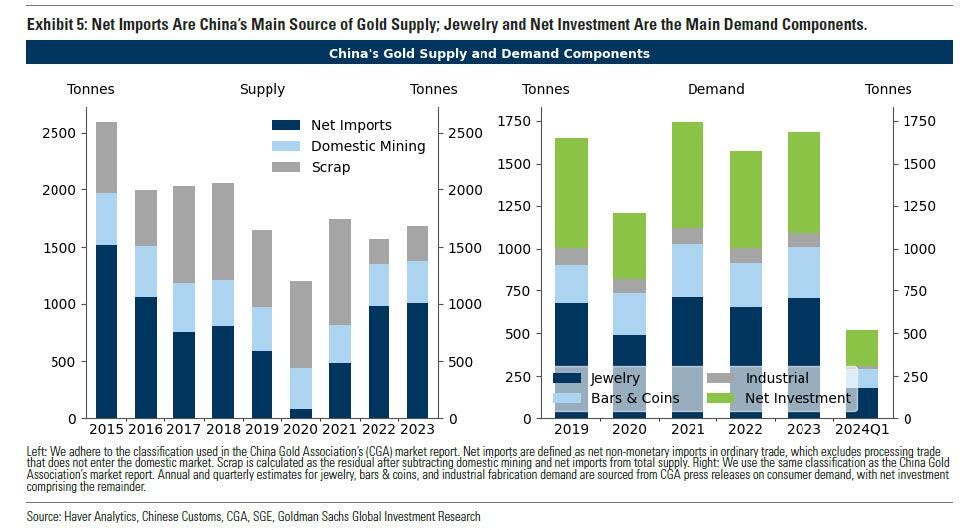

China's gold supply comes from three sources: (1) non-monetary imports in ordinary trade (1,007 tonnes in 2023), its main source of supply, (2) scrap metal, and (3) domestic mining output from the world's largest producer, with approximately 400 tonnes annually. Gold destined for China's domestic private market is channelled through the SGE and must meet strict quality standards, being melted and cast in SGE-approved refineries before being supplied.

Demand

According to figures released by the China Gold Association, Chinese physical demand comprises approximately 40% in jewelry, 20% in bars and coins, and 5% in industrial manufacturing, which together make up wholesale demand, with the remainder allocated to net investment. The chart below shows that Chinese gold demand (based on SGE monthly withdrawals) has retreated from its January peak and is down 16% (3MM, YoY) in June.

Clear supply and demand (mostly) at local level

Due to the relatively insular nature of the Chinese gold market, local and international prices can diverge, with the difference being referred to as the Shanghai-London premium or discount. Given China’s strict export restrictions, any excess supply that induces a discount is ultimately absorbed by increased domestic demand. Conversely, supply shortages induce a premium that destroys demand or encourages an influx of scrap supply. Supply shortages can also be resolved by increased imports, which in turn can affect international prices. Import adjustments are not a guaranteed solution, however, as Chinese authorities closely monitor gold inflows through quarterly import quotas, albeit adjustable based on market conditions. In the second half of 2023, gold import restrictions were tightened, with the local premium reaching over $120 per tonne on 14 September 2023.

Fear, income, yields and prices drive gold demand in China

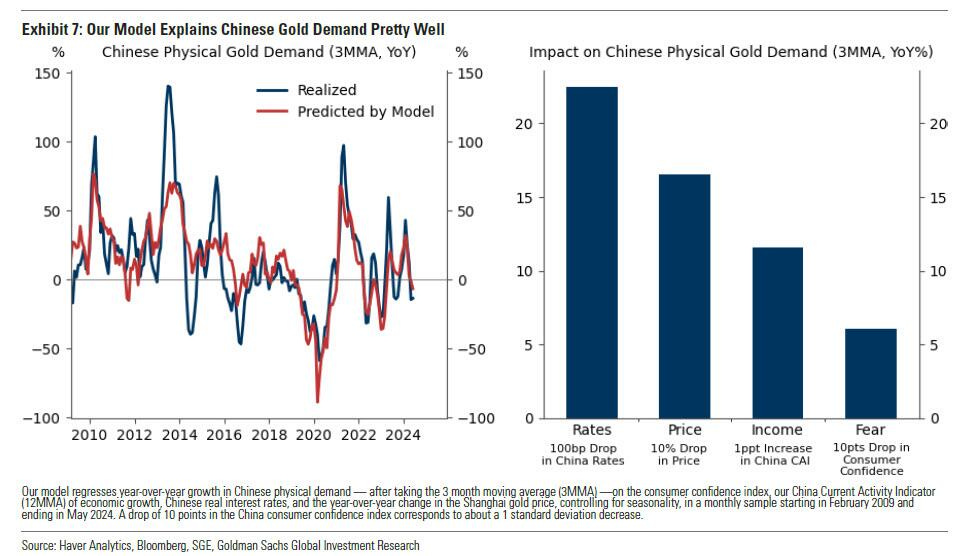

Goldman models Chinese gold demand based on measures of fear, income, Chinese interest rates, and gold prices. The model regresses year-over-year growth in Chinese physical demand (after taking the 3-month moving average (3MMA)) on the consumer confidence index, the China Current Activity Indicator (12MMA) of economic growth, the level of Chinese real interest rates, and year-over-year growth in the Shanghai gold price. The bank finds that fear (measured as low consumer confidence), income/wealth (i.e., our China Current Activity Indicator), low Chinese interest rates, and low gold prices significantly drive Chinese gold demand. As Chart 7 (left) shows, the model explains swings in Chinese gold demand quite well.

Notably, Goldman sees the Chinese market as particularly price-sensitive; the bank estimates that a 10% drop in the Shanghai gold price would increase China's physical gold demand by 16%.

Cyclically soft, structurally intact

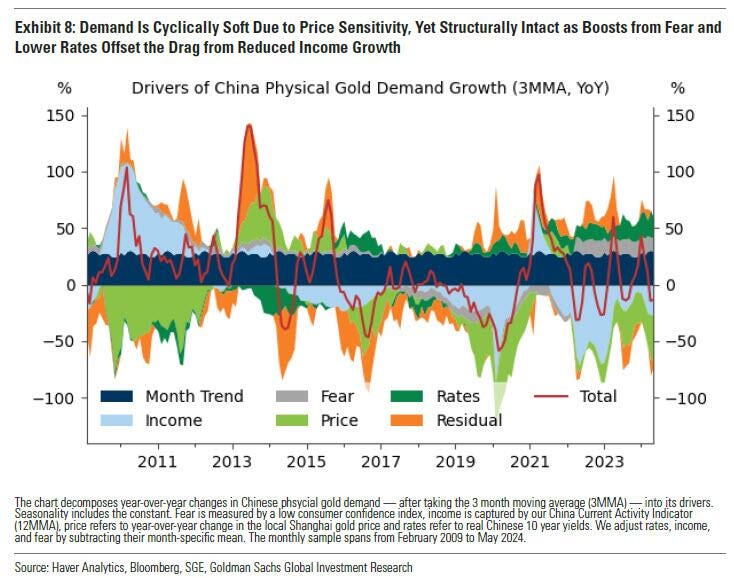

This model also explains the swings in Chinese gold demand over the past 15 years. Goldman concludes that rapid economic growth drove the surge in gold demand in 2010. During the pandemic, high international gold prices and weak economic activity led to a 27% year-over-year drop in demand as price-sensitive Chinese consumers cut back on discretionary spending on gold jewelry (down 27% year-over-year).

While Chinese gold demand is now cyclically weak due to price sensitivity and recent price increases, structural changes leave Chinese gold demand largely unchanged on net because the demand impact of lower trend GDP (income/wealth) growth is largely offset by the boost from lower interest rates and lower confidence (fear) due to real estate issues and economic uncertainties.

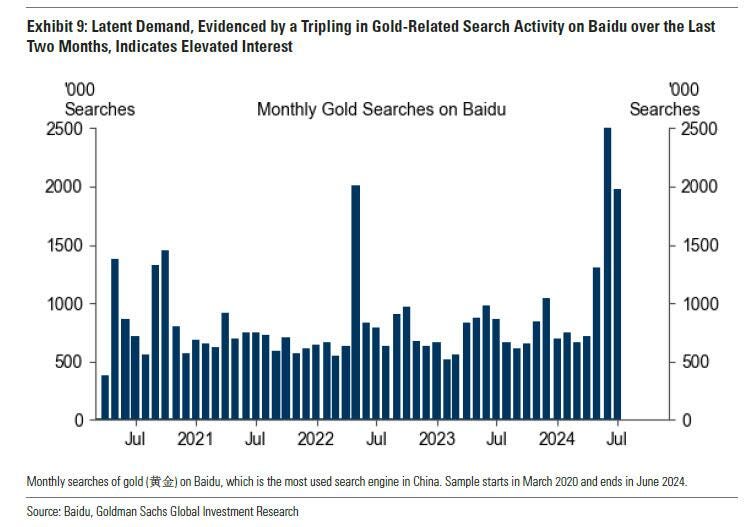

Goldman also finds further evidence of this price sensitivity in the recent shift in demand across gold categories: gold jewelry purchases declined 3% year-over-year in Q1 2024 as consumers cut back on discretionary spending, while demand for more cost-effective bullion and coins rose 27% year-over-year. Furthermore, a tripling of gold-related search activity on Baidu suggests robust latent demand, with a hypothetical large price drop likely to reinvigorate Chinese buying.