BofA SECURITIES | GLOBAL RESEARCH

Gas stocks are high, import coverage is low

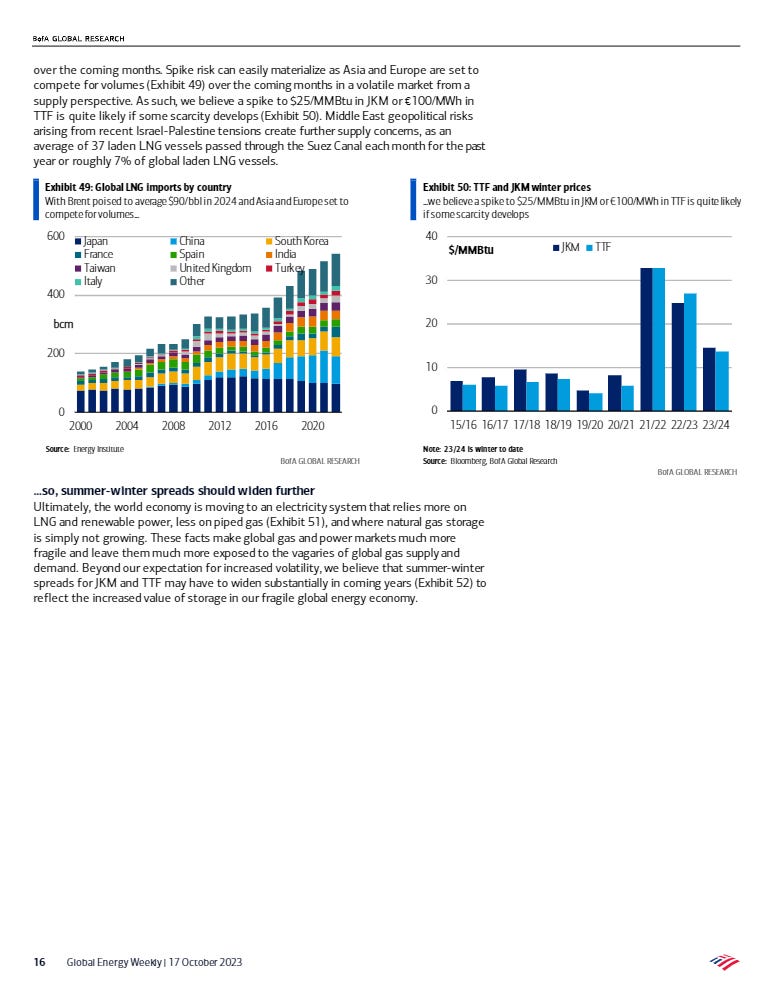

After bottoming out on rising China coal prices, global LNG has shot up recently. Stocks are almost full, but winter demand coverage ratios may be too low to cope with the growing LNG import dependency in Europe and Asia. After all, LNG is the most volatile thermal fuel: very hard to store and transport. As China and Japan continue to buy large LNG volumes near term, competition perpetuates large swings in the TTF-JKM spread to balance the Atlantic and Pacific. The good news is that LNG exports will rise medium-term thanks to the US and Qatar, eventually offsetting recent supply reliability issues in Finland, Israel, or Australia. Longer term, renewable capacity growth and the return of nuclear and hydro may cut power sector LNG demand in Europe and East Asia.

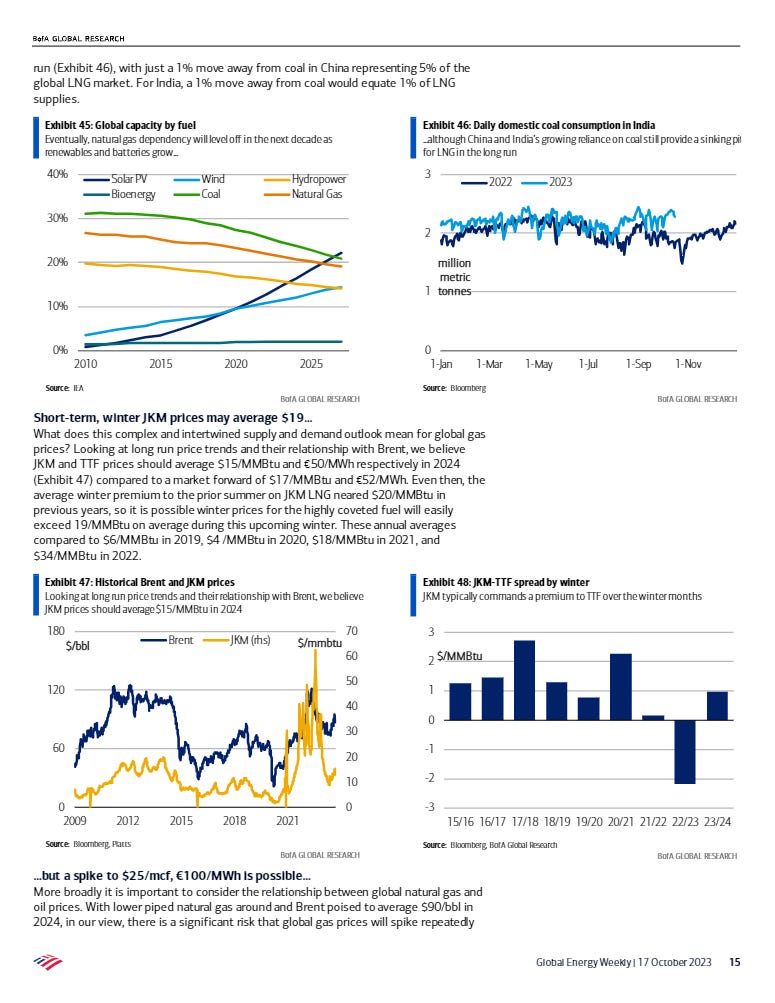

Summer-winter gas spreads should widen

JKM and TTF prices should average $15/MMBtu and €50/MWh respectively in 2024 compared to a market forward of $17/MMBtu and €52/MWh. Even then, risks could materialise due to East-West competition for gas, and a spike to $25/MMBtu in JKM or €100/MWh in TTF is quite likely if winter supply scarcity unfolds. Ultimately, the world is becoming more reliant on LNG and renewable power and less on piped gas. Yet gas storage capacity growth is insufficient. These facts leave gas and power markets much more exposed to the vagaries of LNG supply chains. In addition to increased volatility, we believe JKM and TTF summer-winter spreads may have to widen materially in the coming years to reflect the increased value of storage in a fragile global energy market.

What does Middle East turmoil mean for oil & gas?

The concept of energy fragility quickly brings to mind the current turmoil in the Middle East. Yet Israeli-Palestinian conflicts post 1973 have had a limited impact on energy prices because they were mostly contained. So, the key question for energy is whether the conflict broadens regionally or not. If it does, oil prices could climb above $130/bbl on the risk of a Persian Gulf shutdown. If shipments through Hormuz, a choke point for nearly 20% of the world's oil and LNG, were to shut down for a meaningful period, oil may spike above $250/bbl and LNG may surpass $50/MMBtu. But even if the conflict does not broaden, the US may enforce Iranian oil sanctions, curbing global oil supply by 1-1.5mm b/d in 2024, likely pushing Brent prices above $100/bbl and LNG above $20/MMBtu

Are there any automatic prices stabilizers?

While Saudi Arabia has >2mn b/d of spare capacity and could make up for lost Iranian barrels, recent signaling suggests Saudi is unlikely to unless oil exceeds $100/bbl. In terms of potential impact of higher energy prices globally, we note resource-poor Europe and Japan would likely suffer most. US energy independence means America is less sensitive to an extemal energy price shock, although the US SPR has been greatly depleted during the Ukraine war. Higher oil prices would stoke US inflation too. As the world's biggest energy importer, China may also be hurt, but their growing strategic oil stockpiles can help them temporarily cope with minor Middle East supply disruptions.